Vesting Schedule: Complete Guide for Founders & Employees

A vesting schedule is one of the most important, and most misunderstood, elements of equity compensation. Whether you are a startup founder diluting your own shares, an early employee negotiating an offer, or a CFO designing a company-wide equity plan, understanding how vesting works can mean the difference between retaining your best people and watching them walk out the door with equity they never truly earned.

This guide covers everything you need to know: how vesting schedules work, the different types available, the role of cliff periods, acceleration clauses, and how to design a plan that benefits both your company and your team.

What Is a Vesting Schedule?

A vesting schedule is a timeline that defines when an employee, founder, or other equity holder earns the right to fully own their granted shares or stock options. Rather than receiving 100% of their equity upfront, recipients earn ownership gradually, typically over several years, contingent on continued service or hitting defined milestones.

The core idea is straightforward: equity is a long-term incentive. It should reward people who stick around and contribute to the company’s growth over time, not those who join briefly and leave.

Key Terms to Know

Before diving deeper, it helps to be familiar with a few essential terms:

- Grant date: The date on which equity is officially awarded to an employee or founder.

- Vesting period: The total length of time over which equity is earned. Most commonly four years.

- Cliff: A minimum period that must pass before any equity vests at all.

- Exercise price (strike price): The price at which an employee can purchase their vested stock options.

- Fully vested: The point at which 100% of the granted equity has been earned.

How Does a Vesting Schedule Work?

When a company grants equity to a team member, the shares or options are placed into a vesting schedule. The employee does not own those shares outright, they earn them over time as they remain with the company. If the employee leaves before the schedule is complete, they forfeit whatever portion has not yet vested.

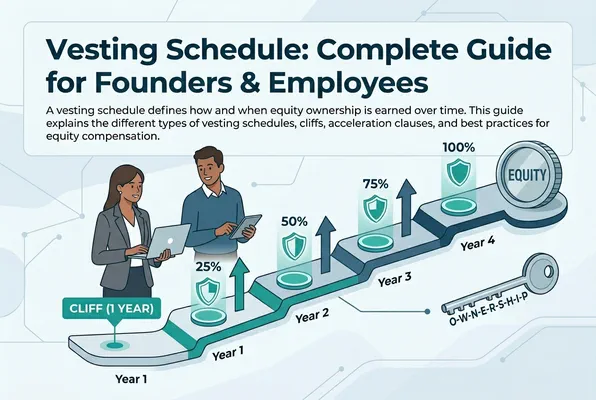

A Standard Example

Imagine an employee is granted 10,000 shares under a standard four-year vesting schedule with a one-year cliff:

- Month 1–12: No shares vest. The employee must complete the full cliff period.

- Month 12: 2,500 shares vest immediately (25% of the total grant).

- Months 13–48: The remaining 7,500 shares vest in equal monthly instalments of approximately 208 shares per month.

If the employee leaves at month 10, they receive nothing. If they leave at month 24, they keep 5,000 shares (the cliff grant plus 12 months of monthly vesting). If they stay all four years, they own all 10,000 shares.

This structure protects the company while still offering meaningful equity incentives to employees who commit to the long term.

Types of Vesting Schedules

There is no single universally correct vesting structure. Companies design their schedules based on their stage, culture, and compensation strategy. Here are the most common types.

Common Types of Vesting Schedules: Cliff vs. Graded Vesting

While time-based vesting schedules are the most common approach, companies generally choose between two main types of vesting structures: cliff vesting and graded vesting. Under a cliff vesting schedule, recipients must complete a defined waiting period before any equity vests. Once that milestone is reached, a significant portion of the grant becomes vested at once. By contrast, a graded vesting schedule allows equity to vest gradually over time, providing more frequent ownership milestones for employees.

Both approaches can be effective depending on the company’s retention goals. A cliff structure strongly encourages employees to remain through a key period, while a graded schedule can create a more continuous sense of progress and reward throughout the vesting period.

Time-Based Vesting

This is the most widely used approach. Equity vests on a fixed schedule tied purely to the passage of time, typically monthly, quarterly, or annually over a defined period. The 4-year monthly vesting with 1-year cliff is the industry standard in venture-backed startups.

Advantages: Simple to understand and communicate to employees - Predictable for financial planning and cap table management - Aligns with typical company growth timelines

Disadvantages: Does not distinguish between high performers and underperformers - An employee can technically “vest in peace” — show up but not contribute meaningfully

Milestone-Based Vesting

Also called performance-based vesting, this approach ties equity ownership to the achievement of specific goals. These milestones might be revenue targets, product launch dates, customer acquisition numbers, or other key performance indicators (KPIs).

Advantages: Directly ties equity rewards to value creation - Highly motivating for goal-oriented individuals - Useful for advisors, contractors, or part-time contributors

Disadvantages: Harder to define fair and objective milestones - Can create tension or disputes if milestone definitions are ambiguous - Complex to administer, especially as company strategy evolves

Hybrid Vesting

Many companies, particularly at later stages, use a combination of time-based and milestone-based vesting. For example, shares might vest on a time schedule, but only if certain company performance benchmarks are also met. This approach is especially common in executive compensation and long-term incentive plans (LTIPs).

Back-Loaded Vesting

Rather than equal monthly increments, back-loaded vesting schedules award more equity in later years. A common structure might vest 10% in year one, 20% in year two, 30% in year three, and 40% in year four. This structure is designed to strongly incentivize long-term retention, though it can feel less rewarding early on.

The Vesting Cliff: Why It Matters

The cliff is arguably the single most important feature of any vesting schedule. It represents the minimum tenure required before a single share or option vests.

Variations of Cliff Vesting Structures

Although the one-year cliff remains the industry standard, companies occasionally adopt vesting structures tailored to specific hiring or retention needs. A 3-year cliff or even a three-year cliff vesting schedule may be used for strategic retention grants, executive compensation packages, or long-term incentive plans where the employer wants participants to stay with the company for a certain number of years before receiving meaningful ownership rights.

Longer vesting arrangements are less common but can be effective in situations where continuity is critical. The vesting schedule determines not only when ownership is earned, but also how strongly the equity program encourages employees to remain committed during periods of rapid company growth or organizational change.

The One-Year Cliff Standard

The 12-month cliff has become the de facto standard in startup equity compensation, particularly in the United States and increasingly in Europe. This convention emerged from the venture capital world as a practical way to protect companies from the consequences of early employee turnover.

Without a cliff, someone who joins and leaves after just a few months could walk away with a small but meaningful stake in the company. That creates issues ranging from a messy cap table to a disgruntled former employee having voting rights or information rights. The cliff eliminates that risk entirely for the first year.

Can You Have a Shorter or Longer Cliff?

While one year is standard, companies do experiment:

- No cliff: Sometimes used for very senior hires or co-founders who are already deeply invested in the company’s success. Rare and generally not recommended for most employees.

- 6-month cliff: Occasionally used in regions or industries where one year feels too long to attract top talent.

- 2-year cliff: Sometimes used for large refresher grants or retention bonuses where the company wants to ensure meaningful commitment before any payout.

Founder Vesting Schedules

Many founders are surprised to learn that their own equity should be subject to a vesting schedule. In fact, when a startup raises its first institutional funding round, investors will almost always require that founder shares be placed on a vesting schedule.

Why Investors Require Founder Vesting

Investors are betting on the founding team as much as the idea. If a co-founder walks away six months after the seed round, they could retain a large block of unvested, or already fully vested, equity, which is deeply problematic. A vesting schedule for founders ensures that their equity is tied to their continued contribution to building the company.

Typical Founder Vesting Structure

Founders often negotiate slightly different terms than employees:

- Vesting period: 4 years is still standard

- Cliff: Sometimes waived for founders given their pre-investment contributions, or replaced with a shorter 6-month cliff

- Credit for past service: Investors may agree to treat a period of time worked before the funding round as already vested, effectively reducing the unvested portion going forward

For example, a founder who has been building the company for 12 months before the seed round might negotiate that their first year is treated as already vested, with the remaining three years of vesting beginning at close of the round.

Co-Founder Vesting: Protecting the Partnership

If you are building a company with co-founders, setting up vesting schedules for everyone from day one is one of the most important legal and structural decisions you will make. Without it, a co-founder who leaves early can take a disproportionate share of the company, demotivating remaining founders and complicating future fundraising.

Acceleration Clauses: Getting Vested Faster

Vesting acceleration provisions allow equity holders to vest faster than the standard schedule under certain circumstances. These clauses are most commonly negotiated by executives and senior employees as part of their offer packages.

Single-Trigger Acceleration

Single-trigger acceleration occurs when a single predefined event causes some or all unvested equity to vest immediately. The most common trigger is a change of control event, meaning an acquisition or merger of the company.

For example, a senior engineer might negotiate that 50% of their unvested options vest automatically upon a company acquisition, regardless of whether they remain with the acquirer.

Double-Trigger Acceleration

Double-trigger acceleration requires two events to occur before unvested equity vests:

- A change of control (acquisition or merger)

- A subsequent qualifying event affecting the employee — typically involuntary termination without cause, significant reduction in role, or being required to relocate

This structure is generally preferred by investors and acquirers because it ensures key employees remain motivated to stay through the transition period rather than vesting everything and immediately leaving.

When to Negotiate Acceleration

If you are joining a company as a senior leader or executive, acceleration clauses are a legitimate and increasingly common part of the negotiation. They provide meaningful downside protection in scenarios where the company is acquired and your role is eliminated. However, they add complexity to the cap table and may be resisted by early-stage founders or small companies who are less familiar with these provisions.

Equity Compensation Vehicles and Vesting

Vesting schedules apply to various forms of equity compensation, and the mechanics can differ slightly depending on the instrument involved.

Stock Options (ISOs and NSOs)

Stock options give the holder the right, but not the obligation, to purchase shares at a fixed price (the exercise price) after they have vested. Once vested, options typically have an expiration date, often 10 years from grant or 90 days after leaving the company.

- Incentive Stock Options (ISOs): Available only to employees in the US. Offer potential tax advantages if held for the required periods.

- Non-Qualified Stock Options (NSOs): Available to employees, advisors, and contractors. Less favorable tax treatment but more flexible.

Understanding Employee Stock Options and Ownership Rights

For employees receiving an employee stock option grant, it is important to understand what vested means in practical terms. Vesting occurs when the employee gains the right to exercise the stock options according to the agreed vesting terms. Once options have vested, the holder generally has the right to buy company shares at the predetermined exercise price, subject to any applicable expiration dates and plan rules.

However, vesting does not automatically mean full ownership of stock. Employees typically gain ownership only after they exercise their stock options and acquire the underlying shares. Understanding the distinction between vesting and ownership helps employees make more informed decisions about when and how to exercise their stock options.

Restricted Stock Units (RSUs)

RSUs represent a promise to deliver actual shares once vesting conditions are met. Unlike options, there is no exercise price, the employee simply receives shares upon vesting. RSUs have become increasingly common at later-stage private companies and are the dominant form of equity compensation at large public technology companies.

RSUs typically vest on a time-based schedule, and taxes are owed at the time of vesting based on the fair market value of the shares received.

Restricted Stock Awards (RSAs)

Unlike RSUs, restricted stock awards grant actual shares immediately, but subject to a vesting schedule and the right of the company to repurchase unvested shares if the employee leaves. RSAs are more common at very early-stage startups where the share price is low, enabling employees to file an 83(b) election with the IRS and potentially reduce future tax liability.

Vesting Schedules in Europe

While the 4-year/1-year cliff structure originated in US startup culture, it has become widely adopted across European startup ecosystems as well. However, there are some notable regional differences to be aware of.

Legal and Tax Considerations

Each country has its own legal framework governing equity compensation, and the tax treatment of stock options and RSUs varies significantly across Europe. Countries like the UK, France, Germany, and the Netherlands each have specific approved schemes (such as the UK’s Enterprise Management Incentive, or EMI) that can offer significant tax advantages when structured correctly.

If you are designing an equity plan for a European company, it is essential to work with legal and tax advisors who understand the local regulatory environment.

VSOP and Phantom Plans

In some European countries, particularly Germany, it can be legally complex or costly to issue actual shares to employees. As a result, Virtual Stock Option Plans (VSOPs) and phantom equity arrangements are common alternatives. These instruments are designed to mimic the economic payoff of real equity without transferring actual ownership, and they also operate on vesting schedules.

Designing an Effective Vesting Schedule for Your Company

If you are a founder or HR leader designing an equity plan, the vesting schedule you choose will have long-lasting implications for your team’s motivation, your cap table, and your ability to attract talent.

Balancing Retention Goals with Flexible Vesting Rules

As organizations mature, they often introduce different vesting structures to support varying talent and compensation objectives. Some companies combine standard vesting schedules with milestone vesting arrangements, while others implement accelerated vesting provisions for senior leaders or key hires. The goal is to balance retention with fairness, ensuring that employees who stay with a company and contribute to long-term success are appropriately rewarded.

When evaluating vesting rules, employers should consider company stage, hiring plans, and the expected years of vesting service for different employee groups. A thoughtful approach to vesting over time can improve employee engagement, strengthen retention, and create a more sustainable equity compensation program for future growth.

Consider Your Company Stage

- Pre-seed and seed: Standard 4-year/1-year cliff for employees. Founder vesting negotiated with investors at Series A. Keep it simple.

- Series A and B: Introduce refresh grants for long-tenured employees. Consider executive acceleration provisions. Think about back-loaded vesting for retention.

- Series C and beyond: More sophisticated equity programs may incorporate performance vesting or hybrid structures tied to company milestones.

Communicate Clearly and Transparently

One of the most common failures in equity compensation is a lack of clear communication. Employees who don’t understand their vesting schedule, the value of their grant, or the mechanics of how their options work are less motivated by that equity — and more likely to make poor decisions when they leave.

Invest in clear documentation, employee education sessions, and tools that help your team model the potential value of their equity under different scenarios.

Manage Your Equity Pool Proactively

Every time you grant equity, you are diluting existing shareholders. It is essential to manage your employee option pool thoughtfully — understanding how much equity you have available, how much has been granted and on what schedules, and how upcoming hiring plans will require additional dilution.

Equity management platforms like Incentrium are designed to simplify exactly this: tracking grants, modeling vesting, simulating exit scenarios, and keeping your cap table accurate and up to date.

Common Mistakes to Avoid with Vesting Schedules

Even experienced founders and HR professionals make avoidable mistakes when designing or managing vesting schedules. Here are the most common:

Skipping Founder Vesting at Formation

The time to set up founder vesting is on day one of forming the company — not when investors demand it at Series A. Setting up mutual vesting from the start creates a fair and stable foundation for your founding team.

Granting Too Much Equity Too Early

Front-loading equity grants to early employees can leave you with an empty option pool before you have hired the key team members you need. Reserve meaningful equity for future critical hires.

Forgetting Post-Termination Exercise Windows

A 90-day window to exercise options after leaving a company is standard but can create serious financial hardship for employees who cannot afford to purchase shares or face a large tax bill. Consider offering extended exercise windows — up to 10 years in some cases — as a more employee-friendly alternative.

Neglecting Refresh Grants

A four-year vesting schedule means long-tenured employees eventually become fully vested. Without refresh grants, their equity incentive disappears, reducing retention power. Building a regular cadence of refresh grants into your equity program helps maintain ongoing alignment.

Failing to Update the Cap Table

Inaccurate or outdated cap tables create problems at every stage of company growth — from fundraising to employee negotiations to exit planning. Using purpose-built equity management software ensures your records remain accurate and audit-ready.

Summary: Key Takeaways

A well-designed vesting schedule is one of the most powerful tools available to founders and companies for attracting, motivating, and retaining the people who will build the business. Here is a quick recap of the essentials:

- Vesting schedules define when equity recipients earn ownership of their granted shares or options over time.

- The 4-year vesting schedule with a 1-year cliff is the industry standard for most startup employees.

- Founders should also be subject to vesting, particularly after institutional fundraising.

- Acceleration clauses — single-trigger or double-trigger — can provide protection in acquisition scenarios and are worth negotiating for senior hires.

- Different equity instruments (stock options, RSUs, RSAs, VSOPs) all interact with vesting schedules in slightly different ways.

- Clear communication and accurate cap table management are just as important as the structure of the schedule itself.

Whether you are crafting your first employee equity plan or revisiting your compensation strategy ahead of a funding round, getting your vesting schedule right is a foundational decision. Tools like Incentrium can help you model, manage, and communicate your equity program with confidence.

FAQ

What is a typical vesting schedule for startup employees?

What happens to my unvested shares if I leave a company?

What is a vesting cliff and how does it protect the company?

Can a vesting schedule be accelerated?

Written by

Dominik KonoldCEO & Founder

Dominik Konold is the CEO and founder of Finidy GmbH, specializing in share-based compensation and treasury accounting. With a background in audit and investment banking, he is a certified Professional Risk Manager (PRMIA) and lectures for the Association of Public Banks and the Academy of International Accounting.

Related Posts

Devest Definition: What Does It Mean to Divest Equity and How Does Devesting Work?

This guide explains the concept of devesting in equity compensation, how it relates to vesting and employee share ownership, and why understanding the conditions under which equity can be lost or reclaimed is essential for employees, founders, and HR professionals.

Cliff Vesting: What It Is and How It Works | Incentrium

Learn what cliff vesting is, how cliff vesting schedules work, and how they differ from graded vesting. A clear guide for employees and startup founders on equity, vesting periods, and employee stock ownership plans.

Vesting Explained: Meaning, Schedules & Examples Guide

Understand what vesting means in ESOP and VSOP contracts: how vesting schedules work, why they matter for employees and startups, and what to watch out for before signing.

Ready to simplify your equity programs?

See how Incentrium helps you manage share-based compensation with ease. Book a demo to learn more.

Book a Demo