What Is a Graded Vesting Schedule? A Complete Guide to Graded Vesting

Employer contributions, stock options, and retirement plan matches can be worth tens of thousands of dollars over a career, but only if you actually own them. That ownership is determined by your vesting schedule, and one of the most common structures you will encounter is graded vesting. Whether you are an employee trying to make smart career decisions or an HR professional designing a competitive compensation package, understanding what graded vesting is and how it works is essential.

This guide breaks down everything you need to know: the mechanics of graded vesting schedules, how they compare to other vesting types, their tax implications, and how to use them strategically.

Understanding Vesting: The Foundation

Before diving into graded vesting specifically, it helps to understand the broader concept of vesting itself.

Vesting is the process by which an employee earns full legal ownership of employer-contributed assets over time. These assets can include:

- 401(k) employer matching contributions

- Pension benefits

- Stock options

- Restricted stock units (RSUs)

- Performance shares

- Profit-sharing contributions

An important distinction: your own contributions — the money you personally put into a 401(k) or the salary you earned — are always 100% yours immediately. Vesting only applies to the portion contributed by your employer.

Vesting schedules serve a dual purpose. For employers, they act as a retention tool, incentivizing employees to stay longer. For employees, they represent a powerful form of deferred compensation that grows in value the longer you remain with a company.

What Is Graded Vesting?

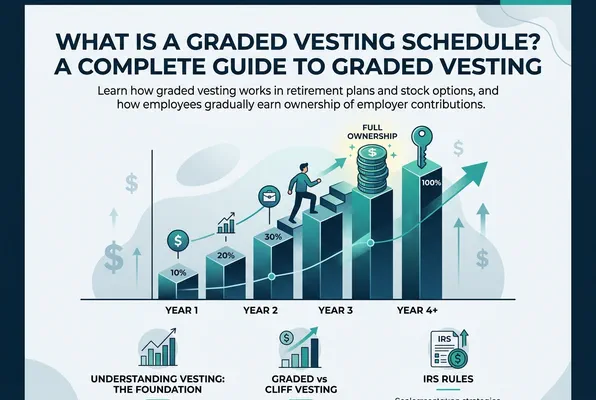

Graded vesting (also called graduated vesting) is a vesting schedule in which an employee gradually earns ownership of employer contributions or equity grants over a defined period. Instead of waiting for a single date to own everything, or nothing, employees accumulate ownership incrementally, typically earning a fixed percentage each year until they reach 100%.

This “step-by-step” approach is one of the most common vesting structures used in both retirement plans and equity compensation programs across industries.

A Simple Example of How Graded Vesting Works

Imagine your employer offers a six-year graded vesting schedule for 401(k) matching contributions. The schedule might look like this:

| Year of Service | Vested Percentage |

|---|---|

| Year 1 | 0% |

| Year 2 | 20% |

| Year 3 | 40% |

| Year 4 | 60% |

| Year 5 | 80% |

| Year 6 | 100% |

If your employer has contributed $10,000 to your retirement account and you leave after three years of service, you would be entitled to 40%, or $4,000. The remaining $6,000 would be forfeited back to the employer.

This graduated approach means employees always walk away with something even if they leave before completing the full vesting period — a key advantage over cliff vesting.

Graded Vesting vs. Other Vesting Types

To fully appreciate what graded vesting offers, it is useful to compare it with the other main vesting structures you are likely to encounter.

Cliff Vesting

Cliff vesting is an all-or-nothing approach. Employees receive zero ownership until a specific date — the “cliff” — at which point they instantly become 100% vested. A common example is a three-year cliff, meaning an employee who leaves after two years and eleven months walks away with nothing from employer contributions.

Key differences:

| Feature | Graded Vesting | Cliff Vesting |

|---|---|---|

| Ownership accumulation | Gradual, year by year | Instant, at cliff date |

| Early departure impact | Partial benefits retained | All employer benefits forfeited |

| Employee risk | Lower | Higher |

| Employer retention leverage | Moderate | Strong (up to the cliff) |

For employees, graded vesting is typically the safer choice. For employers seeking maximum short-term retention, cliff vesting can be more effective, at least until that cliff date passes.

Immediate Vesting

Some employers offer immediate vesting, where employees own employer contributions from day one. While highly attractive to employees, immediate vesting provides no retention incentive for employers and is more common at companies that compete aggressively for talent, such as tech startups or firms with strong cultures.

Hybrid Vesting Schedules

Some companies use a combination: a short cliff period followed by a graded schedule. For example, employees might vest 0% for the first year, then move into a graded vesting structure starting in year two. This protects employers from very short-term turnover while still offering the graduated fairness that graded vesting provides.

IRS Rules Governing Graded Vesting Schedules

For qualified retirement plans like 401(k)s, the IRS sets minimum vesting standards that employers must meet or exceed. Companies cannot make employees wait longer than these minimums to vest.

Vesting Rules in Retirement Plans

Many defined contribution plans, including a profit-sharing plan, may include a plan’s vesting schedule that determines when employer-funded benefits become available. However, personal contributions to a retirement account are always owned by the employee, and those amounts are always 100 percent theirs. Certain arrangements, such as safe harbor contributions and a simple IRA, often require immediate ownership because vesting is required under specific rules. Even if a retirement plan is terminated, an employer cannot generally take away benefits that are already 100 percent vested. Understanding the year of vesting service, years of employment, and any additional year requirements is essential for maximizing retirement benefits.

401(k) Graded Vesting Schedule (IRS Minimum Standards)

Under IRS rules, a graded vesting schedule for employer matching contributions in a 401(k) plan must follow this minimum timeline:

| Years of Service | Minimum Vested Percentage |

|---|---|

| 2 years | 20% |

| 3 years | 40% |

| 4 years | 60% |

| 5 years | 80% |

| 6 years | 100% |

Employers are free to be more generous, offering faster vesting or immediate vesting, but they cannot be less generous than these IRS minimums for employer matching contributions.

For employer non-elective contributions (profit sharing, for example), the IRS may allow slightly different schedules. Always check your Summary Plan Description (SPD) for your specific plan’s rules.

ERISA and Vesting Protections

The Employee Retirement Income Security Act (ERISA) provides the legal framework that protects employee vesting rights. ERISA ensures that:

- Once an employee is vested in a benefit, it cannot be taken away

- Employers must provide clear disclosure of vesting schedules in plan documents

- Vesting schedules must meet minimum federal standards

Understanding your ERISA rights is important if you believe your employer has incorrectly calculated your vested percentage.

Graded Vesting in Equity Compensation Plans

Beyond retirement accounts, graded vesting is extensively used in equity compensation — stock options, RSUs, and other forms of ownership in the company. This is especially prevalent in technology companies, startups, and publicly traded corporations.

Accounting Treatment for Awards With Graded Vesting

When companies grant awards with graded vesting, the accounting treatment can become more complex than for awards with only service conditions that vest all at once. Under accounting standards, organizations must recognize compensation cost throughout the employee’s total requisite service period. The attribution method for awards may require entities to either estimate separate vesting periods for individual tranches or account for the entire award by using a single approach. The selected choice of valuation technique influences how businesses recognize compensation cost on a straight-line basis or allocate cost on a straight-line basis over the total requisite service period.

Graded Vesting with Stock Options

When a company grants stock options with a graded vesting schedule, employees earn the right to purchase a portion of their granted shares each year. For example, if you receive 4,000 stock options with a four-year graded vesting schedule, you might vest 1,000 options per year (25% annually).

This means: - After year 1: You can exercise 1,000 options - After year 2: You can exercise 2,000 options total - After year 3: 3,000 options - After year 4: All 4,000 options are fully vested

Graded Vesting with RSUs

Restricted Stock Units (RSUs) follow a similar pattern. Each tranche of RSUs vests on a schedule, and once vested, the shares are delivered to the employee (often after tax withholding). RSUs with graded vesting are now one of the most common forms of long-term incentive pay at large companies.

Performance-Based Graded Vesting

Some equity plans tie graded vesting to performance metrics rather than (or in addition to) time. Employees might vest a percentage of their award each year only if certain revenue targets, individual performance scores, or operational milestones are met. This combines the gradual ownership of graded vesting with the motivational power of performance pay.

How Graded Vesting Affects Your Tax Situation

Understanding the tax treatment of vested benefits is critical for financial planning.

401(k) Employer Contributions

Employer contributions to a traditional 401(k) are pre-tax. When those funds are vested and eventually distributed (typically in retirement), they are taxed as ordinary income. Early withdrawals before age 59½ typically trigger both income tax and a 10% penalty.

Forfeited unvested contributions do not create a tax event, since you never owned them, you never pay tax on them.

Stock Options

- Incentive Stock Options (ISOs): No regular income tax at exercise, but may trigger Alternative Minimum Tax (AMT). Tax occurs at sale of shares.

- Non-Qualified Stock Options (NSOs): Taxed as ordinary income at exercise on the spread between the exercise price and fair market value.

Graded vesting can actually be advantageous from a tax perspective with NSOs because it spreads taxable income across multiple years rather than concentrating it in one year.

RSUs

RSUs are typically taxed as ordinary income at the time of vesting, when shares are actually delivered. With a graded vesting schedule, this tax event is spread across multiple years, which may help avoid bracket creep compared to a cliff vesting structure.

Section 83(b) Election

For employees receiving restricted stock (not RSUs), a Section 83(b) election allows you to pay taxes on the full grant value upfront at grant date, rather than waiting until vesting. This can be beneficial if you expect the share value to increase significantly. However, this strategy has risks — if you leave before vesting, you do not get a refund of taxes paid on forfeited shares.

The Strategic Value of Graded Vesting for Employers

For HR professionals and business leaders, designing an effective graded vesting schedule requires balancing retention goals with talent attraction.

How Vesting Supports Employee Retention and Financial Growth

A major reason employers implement a type of vesting arrangement is to encourage employee retention. Vesting gives employees a strong incentive to stay with your employer throughout a specific period of time because leaving early could mean leaving free money on the table. As vesting occurs, employees may receive a larger percent each year until they become fully vested. This gradual ownership structure allows employees to gradually earn benefits and employees to gradually earn ownership of valuable compensation that can contribute to their long-term financial security and future retirement savings

Employee Retention

The primary strategic purpose of graded vesting is retention. Employees who are mid-vesting period have a strong financial reason to stay until they are fully vested. This is sometimes called the “golden handcuffs” effect, beneficial compensation structures that make it costly to leave.

With a graded vesting schedule, this retention incentive is sustained over multiple years rather than concentrated at a single cliff point, creating more continuous engagement.

Talent Attraction

At the same time, overly long or restrictive vesting schedules can actually hurt recruitment. Experienced candidates, particularly in competitive industries like technology or finance, often evaluate the vesting terms of an offer carefully. A more generous or accelerated graded vesting schedule can be a meaningful differentiator when competing for top talent.

Forfeiture Planning

Unvested employer contributions that are forfeited by departing employees can often be used to reduce future employer contributions or offset plan administrative costs. Companies with higher turnover rates may factor this into their financial planning around vesting schedules.

Designing a Competitive Schedule

When structuring a graded vesting schedule, consider:

- Your industry benchmarks: What do competitors offer?

- Your average employee tenure: Does your vesting schedule align with realistic career spans at your company?

- The type of compensation: Equity vesting periods (often 4 years) differ from 401(k) vesting norms

- Acceleration provisions: Consider adding change-of-control acceleration clauses that immediately vest employees upon acquisition

What Happens to Your Vesting During Major Life Events?

Leaving Your Job

The most common concern: what happens to your vested and unvested benefits when you resign or are laid off?

- Vested portion: Yours to keep, always. You can roll over vested 401(k) funds to an IRA or new employer’s plan.

- Unvested portion: Forfeited back to the employer.

This is why understanding your vesting schedule before resigning is critical. Waiting a few extra months to cross a vesting threshold could be worth thousands of dollars.

Company Acquisition or Merger

During a merger or acquisition, vesting schedules can change significantly. Some common outcomes include:

- Acceleration: All unvested shares vest immediately (single-trigger or double-trigger acceleration)

- Assumption: The acquiring company assumes the existing vesting schedule

- Replacement: Unvested awards are replaced with new awards from the acquirer on a potentially different schedule

Always review your equity plan documents for change-of-control provisions before any M&A event.

Disability or Death

Most retirement and equity plans have provisions that accelerate vesting in the event of disability or death, ensuring that employees or their beneficiaries receive full credit for their service.

How to Find and Understand Your Vesting Schedule

Not sure what your current vesting schedule looks like? Here is where to find that information:

- 401(k) plans: Check your Summary Plan Description (SPD), which your employer is legally required to provide. Your plan’s online portal (Fidelity, Vanguard, etc.) will also typically show your vesting percentage.

- Equity compensation: Review your grant agreement, stock option plan document, or your company’s equity management platform (such as Carta or Shareworks).

- Employee handbook: HR departments often summarize vesting schedules in onboarding materials or benefits guides.

If anything is unclear, reach out directly to your HR or benefits administrator. You have a right to understand exactly how your vesting schedule works.

Common Vesting Structures and Key Considerations

A company may use a cliff vesting schedule, a four-year vesting schedule, or a graded structure where employees vest 25 percent annually until they are fully vested and remain eligible for benefits. Under a typical year graded approach, ownership increases at the end of year milestones during each calendar year of service. These schedules are common in retirement plans and stock options and are often included as part of a broader benefits package. Employees should review the expected term, any deferral provisions, and their vesting service requirements, particularly when approaching normal retirement age. Consulting a qualified financial advisor can help ensure that important vesting opportunities are not overlooked.

Graded Vesting: Key Takeaways

Understanding what graded vesting is can have a significant impact on your financial decisions, whether you are evaluating a job offer, planning a career move, or building a compensation strategy for your business.

Here are the essential points to remember:

- Graded vesting allows employees to earn ownership of employer-contributed benefits incrementally over time

- It applies to retirement plans (401(k), pension), stock options, RSUs, and profit-sharing programs

- The IRS sets minimum vesting standards for qualified retirement plans, with six-year graded schedules being the most common maximum

- Graded vesting is generally more employee-friendly than cliff vesting, as workers retain partially vested benefits even if they leave early

- Both employees and employers should factor vesting schedules into compensation negotiations, career planning, and financial strategy

- Tax treatment varies by asset type — understanding when a taxable event occurs helps with financial planning

Whether you are just starting your career or you are a seasoned compensation professional, graded vesting is a concept that deserves your full attention. The financial stakes are too high to leave it to chance.

For tools and resources to help manage equity compensation and vesting schedules more effectively, visit incentrium.com .

FAQ

What is graded vesting and how does it differ from cliff vesting?

How long does a typical graded vesting schedule last?

What happens to unvested shares or contributions if I leave my employer early?

Does graded vesting apply to stock options and equity compensation?

Written by

Dominik KonoldCEO & Founder

Dominik Konold is the CEO and founder of Finidy GmbH, specializing in share-based compensation and treasury accounting. With a background in audit and investment banking, he is a certified Professional Risk Manager (PRMIA) and lectures for the Association of Public Banks and the Academy of International Accounting.

Related Posts

Sweat Equity Ventures: Complete Guide to Earning Ownership

Learn how sweat equity helps startups, founders and entrepreneurs build successful businesses by turning skills and effort into ownership.

Warrants vs Options: Key Differences Explained

This guide explains the key differences between warrants and stock options, how they work in practice, and their role in corporate equity structures.

Devest Definition: What Does It Mean to Divest Equity and How Does Devesting Work?

This guide explains the concept of devesting in equity compensation, how it relates to vesting and employee share ownership, and why understanding the conditions under which equity can be lost or reclaimed is essential for employees, founders, and HR professionals.

Ready to simplify your equity programs?

See how Incentrium helps you manage share-based compensation with ease. Book a demo to learn more.

Book a Demo